Yearly Report")

Buyers in Martin Marietta Supplies, Inc. (NYSE:MLM) had a great week, as its shares rose 2.4% to shut at US$540 following the discharge of its full-year outcomes. Martin Marietta Supplies reported in step with analyst predictions, delivering revenues of US$6.8b and statutory earnings per share of US$18.82, suggesting the enterprise is executing nicely and in step with its plan. Following the consequence, the analysts have up to date their earnings mannequin, and it might be good to know whether or not they suppose there’s been a robust change within the firm’s prospects, or if it is enterprise as typical. With this in thoughts, we have gathered the newest statutory forecasts to see what the analysts predict for subsequent yr.

View our newest evaluation for Martin Marietta Supplies

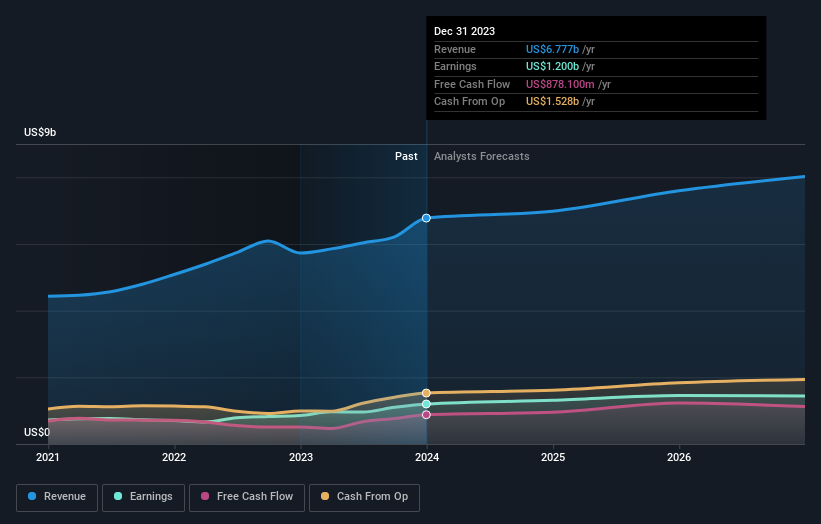

Following the newest outcomes, Martin Marietta Supplies’ 16 analysts are actually forecasting revenues of US$6.98b in 2024. This might be a passable 3.0% enchancment in income in comparison with the final 12 months. Per-share earnings are anticipated to build up 8.8% to US$21.11. Earlier than this earnings report, the analysts had been forecasting revenues of US$7.31b and earnings per share (EPS) of US$20.90 in 2024. The consensus appears possibly a little bit extra pessimistic, trimming their income forecasts after the newest outcomes despite the fact that there was no change to its EPS estimates.

The typical worth goal was regular at US$560even although income estimates declined; seemingly suggesting the analysts place a better worth on earnings. It may be instructive to take a look at the vary of analyst estimates, to guage how totally different the outlier opinions are from the imply. At present, essentially the most bullish analyst values Martin Marietta Supplies at US$642 per share, whereas essentially the most bearish costs it at US$350. There are positively some totally different views on the inventory, however the vary of estimates shouldn’t be large sufficient as to suggest that the scenario is unforecastable, in our view.

One approach to get extra context on these forecasts is to take a look at how they examine to each previous efficiency, and the way different corporations in the identical business are performing. We’d spotlight that Martin Marietta Supplies’ income development is predicted to sluggish, with the forecast 3.0% annualised development price till the tip of 2024 being nicely under the historic 10% p.a. development during the last 5 years. Examine this in opposition to different corporations (with analyst forecasts) within the business, that are in combination anticipated to see income development of 6.3% yearly. Factoring within the forecast slowdown in development, it appears apparent that Martin Marietta Supplies can be anticipated to develop slower than different business individuals.

The Backside Line

An important factor to remove is that there is been no main change in sentiment, with the analysts reconfirming that the enterprise is performing in step with their earlier earnings per share estimates. On the unfavourable facet, in addition they downgraded their income estimates, and forecasts suggest they are going to carry out worse than the broader business. Even so, earnings per share are extra necessary to the intrinsic worth of the enterprise. There was no actual change to the consensus worth goal, suggesting that the intrinsic worth of the enterprise has not undergone any main modifications with the newest estimates.

With that in thoughts, we would not be too fast to come back to a conclusion on Martin Marietta Supplies. Lengthy-term earnings energy is way more necessary than subsequent yr’s income. We have now forecasts for Martin Marietta Supplies going out to 2026, and you’ll see them free on our platform right here.

It may additionally be price contemplating whether or not Martin Marietta Supplies’ debt load is acceptable, utilizing our debt evaluation instruments on the Merely Wall St platform, right here.

Have suggestions on this text? Involved concerning the content material? Get in contact with us straight. Alternatively, e mail editorial-team (at) simplywallst.com.

This text by Merely Wall St is common in nature. We offer commentary primarily based on historic information and analyst forecasts solely utilizing an unbiased methodology and our articles usually are not meant to be monetary recommendation. It doesn’t represent a suggestion to purchase or promote any inventory, and doesn’t take account of your goals, or your monetary scenario. We intention to carry you long-term centered evaluation pushed by basic information. Observe that our evaluation might not issue within the newest price-sensitive firm bulletins or qualitative materials. Merely Wall St has no place in any shares talked about.