Inventory’s Latest Efficiency Being Led By Its Engaging Monetary Prospects?")

Martin Marietta Supplies’ (NYSE:MLM) inventory is up by a substantial 23% over the previous three months. For the reason that market often pay for a corporation’s long-term fundamentals, we determined to check the corporate’s key efficiency indicators to see in the event that they might be influencing the market. On this article, we determined to concentrate on Martin Marietta Supplies’ ROE.

ROE or return on fairness is a great tool to evaluate how successfully an organization can generate returns on the funding it obtained from its shareholders. Put one other manner, it reveals the corporate’s success at turning shareholder investments into earnings.

View our newest evaluation for Martin Marietta Supplies

How Is ROE Calculated?

The system for ROE is:

Return on Fairness = Internet Revenue (from persevering with operations) ÷ Shareholders’ Fairness

So, primarily based on the above system, the ROE for Martin Marietta Supplies is:

15% = US$1.2b ÷ US$8.0b (Based mostly on the trailing twelve months to December 2023).

The ‘return’ refers to an organization’s earnings over the past yr. One other manner to think about that’s that for each $1 value of fairness, the corporate was in a position to earn $0.15 in revenue.

What Is The Relationship Between ROE And Earnings Development?

To this point, now we have realized that ROE measures how effectively an organization is producing its earnings. Based mostly on how a lot of its earnings the corporate chooses to reinvest or “retain”, we’re then in a position to consider an organization’s future capability to generate earnings. Assuming every little thing else stays unchanged, the upper the ROE and revenue retention, the upper the expansion fee of an organization in comparison with firms that do not essentially bear these traits.

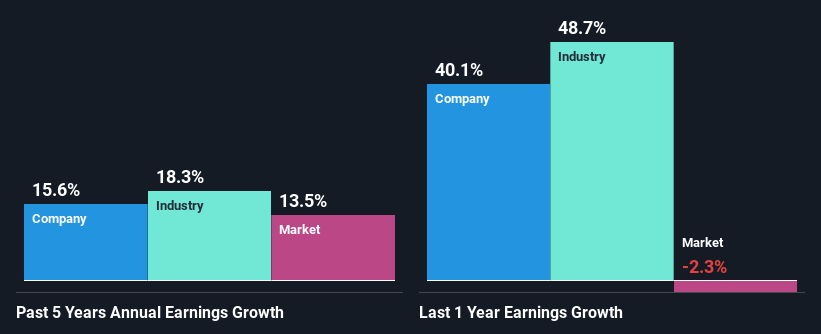

A Aspect By Aspect comparability of Martin Marietta Supplies’ Earnings Development And 15% ROE

At first look, Martin Marietta Supplies appears to have an honest ROE. And on evaluating with the business, we discovered that the the common business ROE is comparable at 14%. This in all probability goes a way in explaining Martin Marietta Supplies’ average 16% development over the previous 5 years amongst different components.

Subsequent, on evaluating Martin Marietta Supplies’ internet earnings development with the business, we discovered that the corporate’s reported development is just like the business common development fee of 18% over the previous couple of years.

Earnings development is a large consider inventory valuation. It’s necessary for an investor to know whether or not the market has priced within the firm’s anticipated earnings development (or decline). Doing so will assist them set up if the inventory’s future seems to be promising or ominous. Has the market priced sooner or later outlook for MLM? You will discover out in our newest intrinsic worth infographic analysis report.

Is Martin Marietta Supplies Utilizing Its Retained Earnings Successfully?

Martin Marietta Supplies’ three-year median payout ratio to shareholders is nineteen% (implying that it retains 81% of its earnings), which is on the decrease aspect, so it looks like the administration is reinvesting earnings closely to develop its enterprise.

Moreover, Martin Marietta Supplies has paid dividends over a interval of not less than ten years which implies that the corporate is fairly critical about sharing its earnings with shareholders. Present analyst estimates counsel that the corporate’s future payout ratio is anticipated to drop to 12% over the following three years. Nonetheless, the corporate’s ROE is just not anticipated to alter by a lot regardless of the decrease anticipated payout ratio.

Abstract

On the entire, we really feel that Martin Marietta Supplies’ efficiency has been fairly good. Notably, we like that the corporate is reinvesting closely into its enterprise, and at a excessive fee of return. Unsurprisingly, this has led to a formidable earnings development. With that mentioned, the newest business analyst forecasts reveal that the corporate’s earnings development is anticipated to decelerate. To know extra concerning the firm’s future earnings development forecasts check out this free report on analyst forecasts for the corporate to seek out out extra.

Have suggestions on this text? Involved concerning the content material? Get in contact with us instantly. Alternatively, e-mail editorial-team (at) simplywallst.com.

This text by Merely Wall St is common in nature. We offer commentary primarily based on historic information and analyst forecasts solely utilizing an unbiased methodology and our articles aren’t meant to be monetary recommendation. It doesn’t represent a advice to purchase or promote any inventory, and doesn’t take account of your goals, or your monetary scenario. We goal to deliver you long-term targeted evaluation pushed by elementary information. Notice that our evaluation could not issue within the newest price-sensitive firm bulletins or qualitative materials. Merely Wall St has no place in any shares talked about.