Romanian residents’ web wealth has elevated over the previous 20 years, however residents have low ranges of financial savings and few monetary belongings—suggesting that monetary schooling, and long-term planning and resilience haven’t progressed equally quick. A major a part of the just lately amassed wealth is in actual property, as Romanians have a transparent historic choice for proudly owning their homes or flats. Regardless of the rise in general wealth, Romanians have far fewer monetary belongings than their fellow Central and Western Europeans and the nation has one of many lowest financial savings charges within the area. When Romanians save, they have an inclination to choose low-risk, low-return choices akin to money, present accounts, and deposits. Basically, Romanians have little belief in each private and non-private pensions, and solely round 3 p.c of the inhabitants put money into voluntary monetary belongings akin to pensions or mutual funds.

This text attracts on the findings of a client survey carried out by McKinsey in Spring 2022 that make clear Romanians’ attitudes towards cash, saving, and monetary planning that will clarify these developments. The survey focused the city inhabitants, with various ranges of schooling, starting from 18 to 65 years of age.

The survey helps international post-pandemic proof that there’s a rise in saving conduct, or a minimum of an intention to avoid wasting extra. Nevertheless, round 60 p.c of Romanians surveyed say they fail to stay to their financial savings objectives. This can be as a consequence of lack of funds. It is also as a result of they lack the mandatory monetary schooling, or entry to dependable monetary recommendation, to assist them perceive tips on how to save or make investments. This example is especially pronounced and difficult within the lower-income and lower-educated segments of the inhabitants.

Shifting ahead, Romanians may leverage the general enhance in wealth, and better earnings ranges, to construct monetary safety in a approach that will enable for higher particular person and collective stability. On a nationwide degree, this might flip the nation’s sustained progress into long-term prosperity. It will take a change in mindset and conduct. And such change could also be tough to attain at scale on a person degree. There are alternatives for all stakeholders—together with shoppers, monetary establishments, and the state—to work collectively to extend monetary consciousness and schooling. These options require collaboration, and concrete measures and actions, and can probably achieve success provided that constructed successfully round shoppers’ wants and expectations.

Web wealth is growing however monetary wealth stays low

The Romanian financial system has adopted an upward pattern and the web wealth of the Romanian inhabitants has elevated greater than eight occasions over the previous 20 years, based on the Nationwide Financial institution of Romania. Disposable earnings elevated considerably between 2000 and 2020, as Romania had the very best annual progress in disposable earnings per capita in Europe on this interval, at 10 p.c. This allowed Romania to return near the degrees of disposable earnings per capita in additional superior Central European international locations, closing the hole from 60 p.c 20 years in the past, to round 15 p.c in the present day. Many Romanians have invested their wealth in actual property; actually, over 95 p.c of Romanian adults personal an condo or a home, primarily based on Eurostat information. Regardless of this financial progress and a tradition of funding in actual property, Romanians’ web monetary belongings haven’t saved tempo with the rise in general wealth (Exhibit 1).

Between 2000 and 2020, Romania confirmed robust progress in disposable earnings per capita and received near the values seen in Central and Western European international locations, however residents didn’t redirect the additional earnings into financial savings. Romania has one of many lowest ranges of private monetary wealth in comparison with different Central and Western European international locations, at 36 p.c of GDP—which is roughly half the Central European common, based on McKinsey Panorama information. Monetary wealth per capita is round $5,000. By comparability, Hungary’s monetary wealth penetration fee is at 72 p.c of GDP, with a per-capita monetary wealth of $12,000.

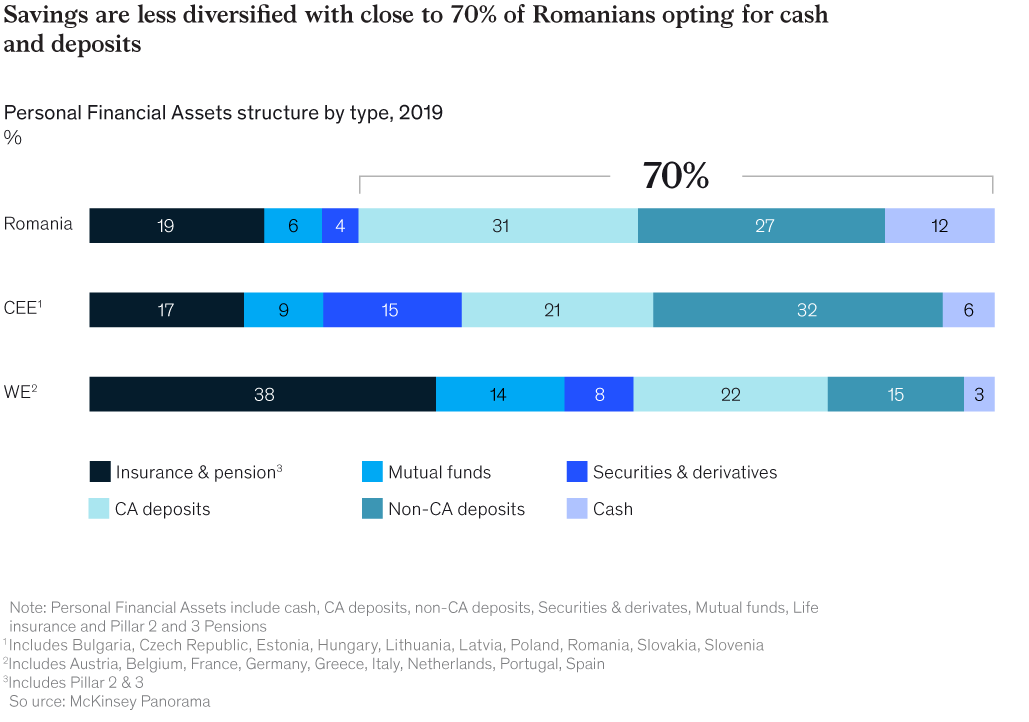

When current, Romanians’ financial savings are largely in money and deposits. Money, cash held in present accounts, and deposits make up 70 p.c of private monetary belongings, in comparison with 59 p.c in Central Europe and 40 p.c in Western Europe. Romanians have a tendency to carry two to 4 occasions more money when in comparison with regional friends and customarily don’t make use of subtle funding merchandise akin to mutual funds, securities and derivatives (Exhibit 2).

Solely a really restricted a part of Romanian grownup inhabitants have invested in a voluntary monetary asset—round 3 p.c in mutual funds, and fewer than 2 p.c in pillar 3 pensions, primarily based on Nationwide Financial institution of Romania information. The extent of general investments in insurance coverage and pension merchandise is near that seen in Central Europe (just below 20 p.c of private monetary belongings) however is comparatively low in comparison with Western European international locations.

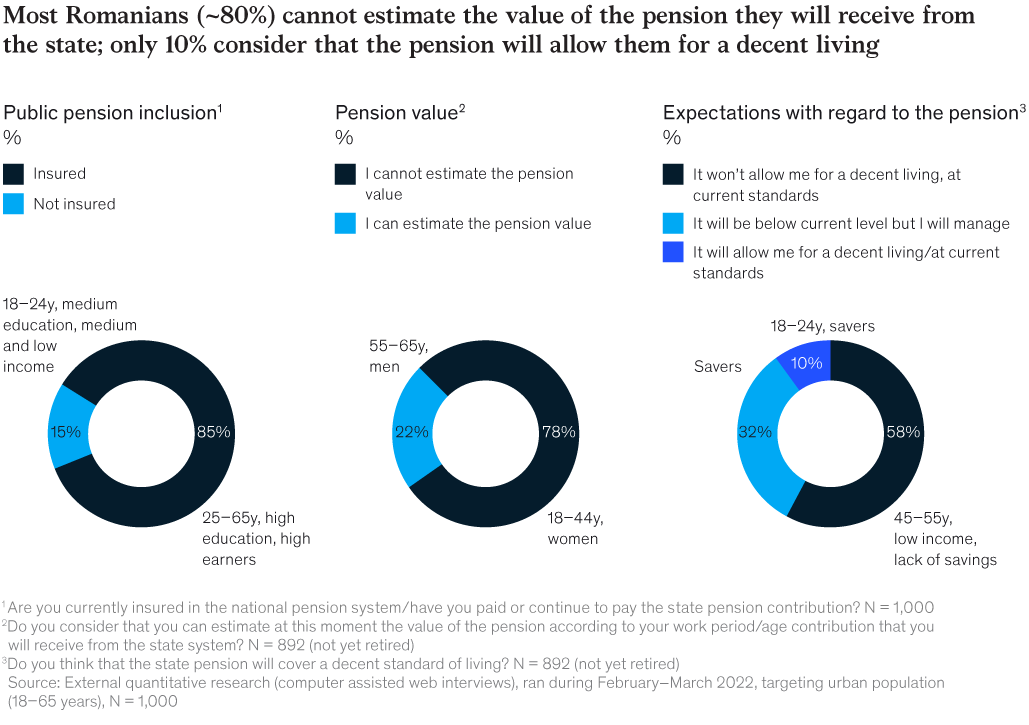

Moreover, it appears that evidently Romanians usually lack religion in each private and non-private pensions. The survey discovered that just one in 5 Romanians belief the general public pension system and just one in 4 belief the privately-managed one. Moreover, 80 p.c of respondents couldn’t estimate the worth of the pension they are going to obtain from the state, and 90 p.c anticipate that their pension will likely be inadequate for them to take care of their way of life publish retirement (Exhibit 3). Lastly, solely 28 p.c of Romanians declared that they plan their retirement proactively.

Many Romanians plan to avoid wasting or make investments extra, however lack the help to take action

The COVID-19 pandemic boosted financial savings charges internationally. This may occasionally have been as a consequence of an absence of spending choices throughout pandemic-related restrictions together with heightened fears round monetary instability. The pandemic elevated consciousness amongst shoppers of the significance of saving; and financial savings elevated globally, together with in Romania. However this momentum is tough to take care of as spending restrictions have eased and excessive inflation has began to dent buying energy.

Regardless of the pandemic-related enhance in financial savings, the survey indicated that just one in 4 Romanians stated that they’ve managed to maintain up with their pandemic-induced saving behaviors. This example is pushed by lack of funds or as a result of they lack the monetary schooling or help to assist them save. As an example, solely 15 p.c of respondents stated that they had attended monetary teaching programs, and just below 30 p.c stated that their households taught them tips on how to make investments.

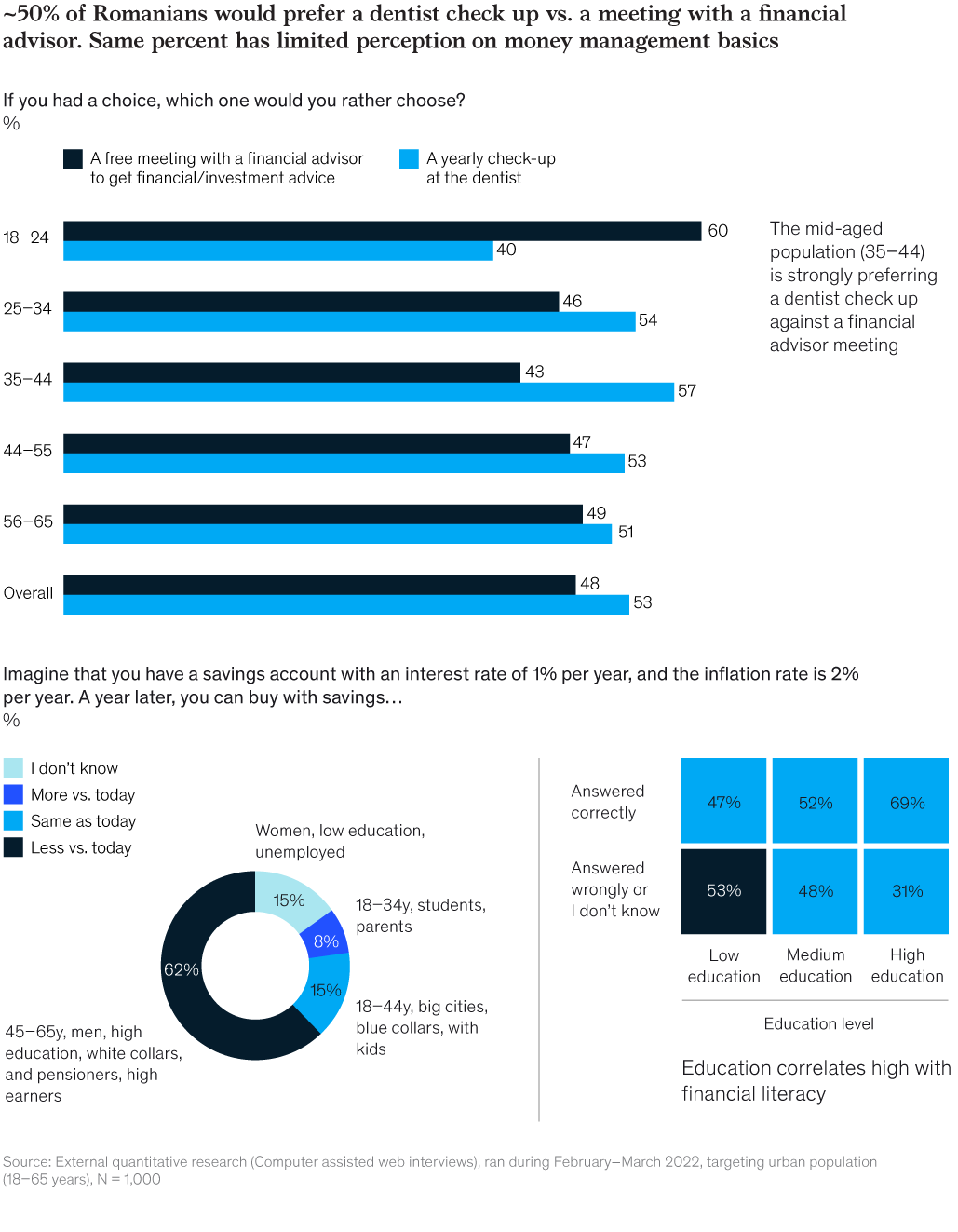

Romanians have long-held attitudes towards saving and monetary planning that have an effect on how they select to avoid wasting or make investments. As an example, though many Romanians want to save extra, they’re hesitant about monetary planning. Actually, barely over half of respondents stated they might reasonably schedule a yearly check-up at a dentist than attend a free assembly with a monetary advisor. After all, dental check-ups are vital, whereas saving is voluntary, however the sentiment is evident: Romanians are hesitant to hunt monetary recommendation even whether it is free. The same share had problem with basic money-management ideas akin to understanding the impact that inflation would have on financial savings (Exhibit 4).

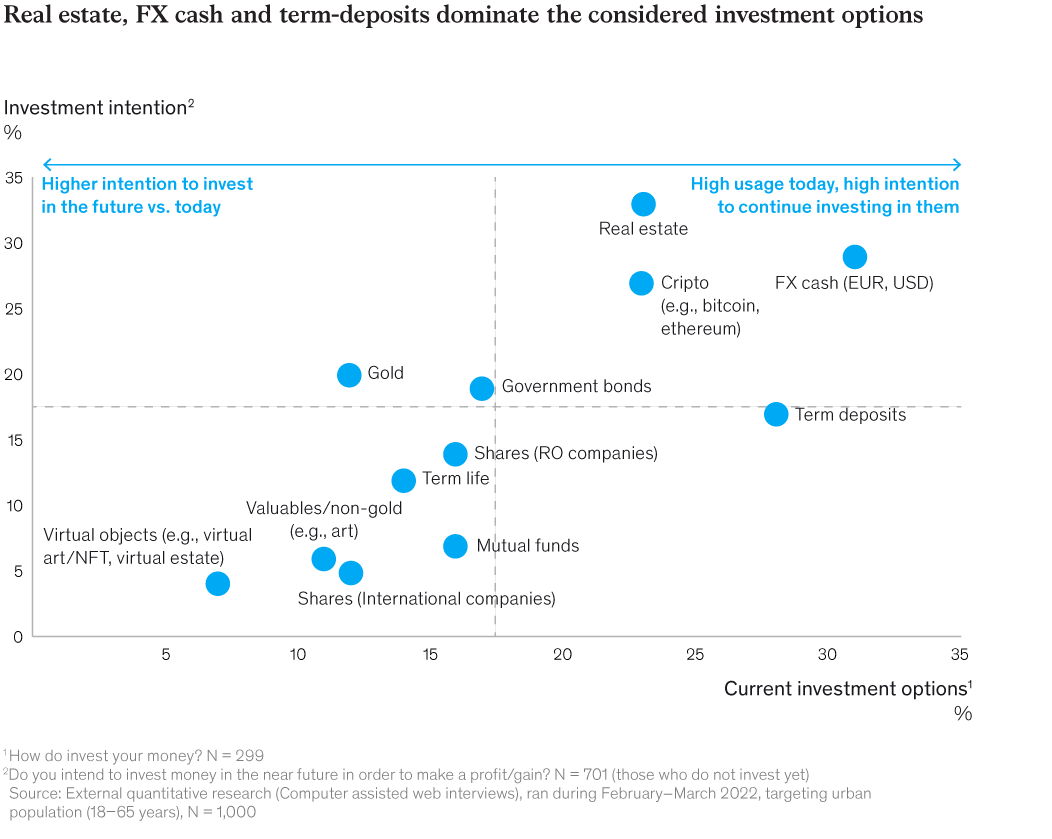

This lack of belief in monetary recommendation, and low ranges of monetary schooling, additionally have an effect on how Romanians select to speculate. The survey discovered that respondents are both threat averse and select low-risk, low-return belongings akin to overseas forex and time period deposits or go for speculative investments akin to cryptocurrencies (Exhibit 5).

Despite the fact that Romanians are making these funding choices, the survey signifies that they’re making them on their very own. A person’s private circle of household and associates takes priority as a reputable supply of knowledge concerning cash administration over monetary establishments or consultants akin to monetary advisors—and 75 p.c of respondents declare to handle their investments alone. Solely 20 p.c imagine that banks provide dependable monetary recommendation and solely 18 p.c examine with their financial institution when making a money-related determination.

Along with a risk-averse angle, an absence of monetary data, and distrust of establishments or people who may present monetary recommendation, many Romanians face different challenges that stop them from saving or investing. The mixture of low earnings and excessive debt is a major problem. This example is especially dire for low-income, low-education segments of the inhabitants. The survey reveals that solely 26 p.c of the much less educated phase handle to avoid wasting in any respect, in comparison with the nationwide common of 63 p.c who handle to avoid wasting sometimes or month-to-month. Those that point out that they save each month, however not a set quantity—32 p.c—are likely to stay in mid-size cities and have increased schooling ranges.

The youthful segments of the inhabitants appear equally challenged to deal with monetary investments. Despite the fact that 31 p.c of the 18- to 24-year-old phase surveyed are nonetheless financially dependent, they plan to avoid wasting or make investments. However they too lack monetary schooling and present even increased ranges of threat adversity than common.

There’s a robust consensus amongst respondents that the state ought to provide extra help for the inhabitants to avoid wasting greater than they presently do, as 65 p.c of respondents declared that the state ought to get extra concerned in serving to the inhabitants to avoid wasting or make investments by providing incentives. As a lot as 60 p.c felt that banks or insurers must also get extra concerned in serving to the inhabitants to avoid wasting by providing counselling and recommendation, and offering merchandise that go well with clients’ wants. Romanians additionally imagine that households ought to play a bigger function in offering monetary schooling for his or her kids and that the education system must also help on this regard.

Alternatives to construct wealth exist

Romanians may construct on the latest momentum of elevated financial savings, and they’ll want wider help, from a wide range of stakeholders, to assist them construct and diversify their private wealth. Change will likely be tough to attain at a person degree. There are alternatives for monetary establishments, the state, and shoppers to collaborate find methods to extend monetary schooling, present services or products that meet shoppers’ wants, and finally construct a tradition of monetary consciousness to spice up private wealth, on high of current efforts, whereas scaling people who proved environment friendly.

There are examples of initiatives and finest practices in different elements of Europe which have offered accessible monetary schooling. The next 4 examples spotlight methods during which the boundaries and challenges of monetary inclusion may be overcome. In Belgium, academic web sites focused at potential traders provide easy-to-understand recommendation, akin to ideas for taking step one towards investing within the inventory market or key pointers for understanding pensions. There are additionally platforms for newbie traders that designate the fundamentals of investing and supply an summary of potential funding choices. Such platforms are made accessible as they’re promoted by way of social media. Moreover, the Belgian schooling system performs a component in primary monetary schooling as kids from the primary to the sixth grade obtain monetary coaching as a part of their most important curriculum.

Monetary establishments have additionally discovered methods to assist new shoppers start to construct their monetary wealth. For instance, one German asset administration agency develops merchandise particularly to assist first-time traders convert their deposits into funding merchandise and makes use of a defensive asset allocation technique to reduce threat and supply modest progress, which is commonly engaging to risk-averse first-time traders.

One other funding administration agency noticed its funding merchandise develop by 10 p.c a 12 months by creating a complete vary of merchandise to go well with buyer wants, together with multi-asset merchandise and pension plans. The agency’s variety of financial savings plans, lots of which have been opened by the youthful technology, elevated by round 40 p.c between 2020 and 2021. Key success elements for this progress embody offering shoppers with in depth help providers, akin to enterprise planning and administration recommendation, and increasing the methods during which the agency engages with its clients, together with gross sales occasions and analogue and digital channels. The agency additionally developed a direct-to-consumer and business-to-business-for-consumer (B2B4C) platform that gives digital recommendation to each finish shoppers and monetary advisors.

A nationwide financial institution offered a method to educate members of the general public, together with kids and college college students, on monetary issues. The financial institution launched a portal containing sources and knowledge on a wide range of subjects together with household funds, monetary planning, financial savings, and funding rules. It additionally offered monetary schooling actions in colleges and academic facilities, and hosted webinars for college college students. So far, over 30,000 college students have attended monetary literacy lectures, over 8,000 kids have handed the initiative’s monetary literacy quiz, and greater than 14,000 kids have acquired monetary literacy train books.

By drawing on these successes in different international locations, Romanian stakeholders may collaborate to enhance product choices, enhance the standard and availability of monetary schooling and recommendation, and work with the general public to assist them attain their objectives of saving and investing. Public establishments, monetary establishments, and the schooling sector may discover methods to extend entry to monetary literacy, as an example by providing packages in colleges, and making current initiatives more-widely accessible. Monetary establishments may modify merchandise to enchantment to a youthful demographic, as an example by way of gamification, and monetary advisors may method the topical topic of inflation and clarify clearly to shoppers how inflation is prone to have an effect on their buying energy and financial savings, and the way monetary merchandise with implicit or express inflation safety could be useful.

However change could not occur within the brief time period, notably when low earnings and excessive debt are drivers of low financial savings charges. However broader attitudes and behaviors akin to threat aversion and distrust may be overcome by way of higher monetary consciousness, and entry to dependable data.

Such efforts may have important constructive implications for particular person shoppers, and for the nation. If Romanians have been to make financial savings a precedence, supported by related private and non-private initiatives, this might result in a cumulative contribution of €575 billion to the nation’s GDP by 2050 (in actual phrases, listed to 2010), based on our evaluation. On this situation, Romania would attain the present degree of financial savings within the Czech Republic, for instance. By comparability, this worth is roughly the present GDP of Poland (at €520 billion in 2010 costs).

By growing financial savings, and redirecting them to investments, Romania has a possibility to extend GDP by a further 10 p.c by 2050—when in comparison with the anticipated enhance in GDP if no motion is taken. Doing so wouldn’t solely enhance particular person’s web wealth, however have constructive results on the labor market, productiveness, and innovation. Such an method would definitely be a passport to higher prosperity for future generations.