As of October 04, 2023, Martin Marietta Supplies Inc (NYSE:MLM) has seen a every day achieve of 1.73%, and a 3-month lack of 10.31%. With an Earnings Per Share (EPS) of 15.24, the query arises: Is the inventory pretty valued? On this article, we delve into an in depth valuation evaluation of Martin Marietta Supplies, offering worthwhile insights for buyers. Learn on for a complete understanding of the corporate’s intrinsic worth.

A Snapshot of Martin Marietta Supplies Inc (NYSE:MLM)

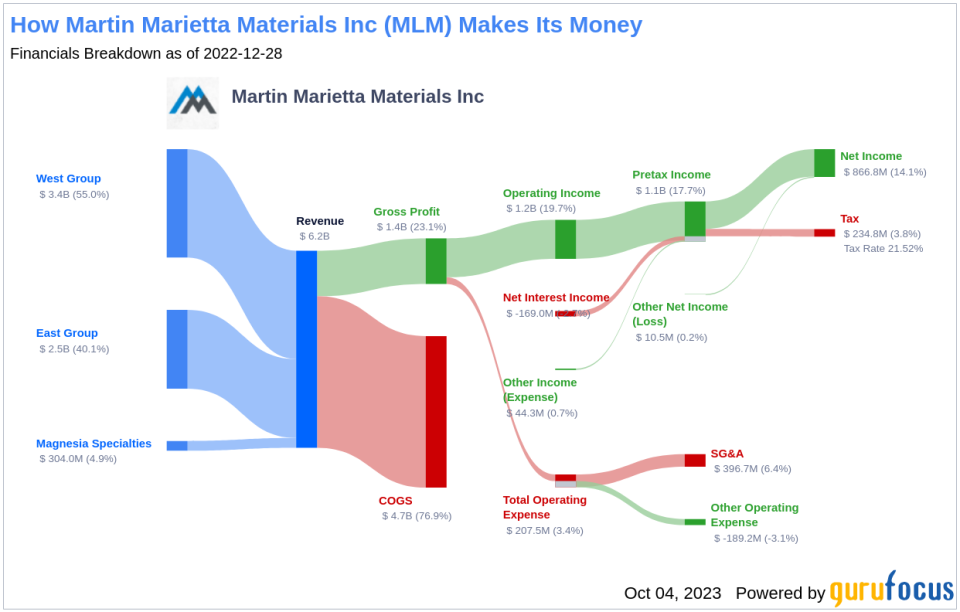

Martin Marietta Supplies is likely one of the largest producers of building aggregates in the USA. The corporate bought 207 million tons of aggregates in 2022, with its most important markets being Texas, Colorado, North Carolina, Georgia, and Florida. Apart from producing cement in Texas, Martin Marietta Supplies additionally makes use of its aggregates in its asphalt and ready-mixed concrete companies. Moreover, the corporate’s magnesia specialties enterprise produces magnesia-based chemical merchandise and dolomitic lime.

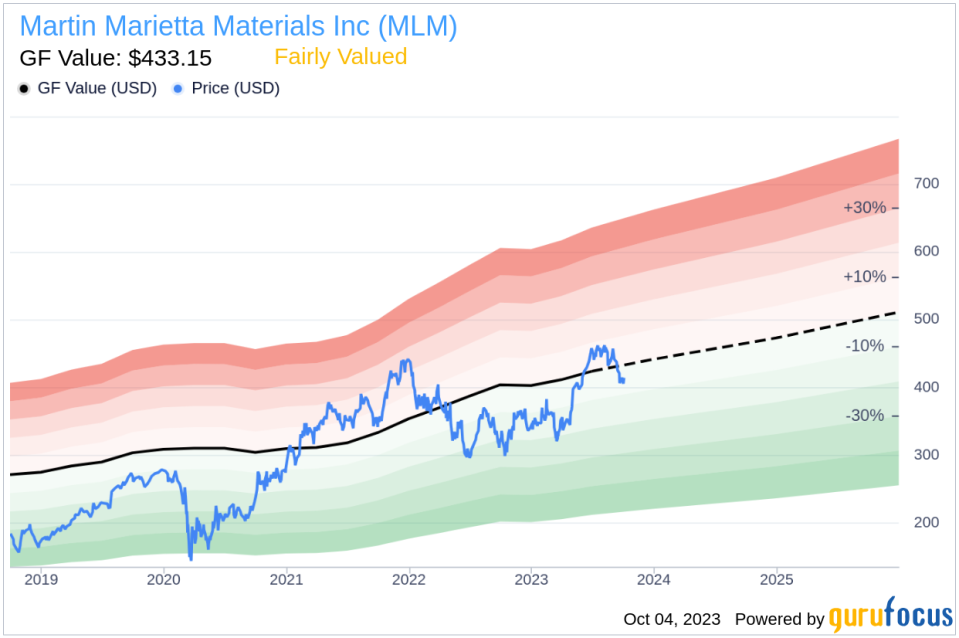

With a inventory worth of $411.36, Martin Marietta Supplies has a market cap of $25.40 billion. The corporate’s GF Worth, a proprietary measure of a inventory’s intrinsic worth, stands at $433.15, indicating that the inventory is pretty valued.

Understanding GF Worth

The GF Worth represents the present intrinsic worth of a inventory, derived from GuruFocus’ unique methodology. The GF Worth Line gives an summary of the honest worth at which the inventory needs to be traded. It’s calculated primarily based on historic multiples, GuruFocus adjustment issue primarily based on the corporate’s previous returns and progress, and future enterprise efficiency estimates.

In response to GuruFocus’ valuation methodology, Martin Marietta Supplies (NYSE:MLM) is estimated to be pretty valued. If the inventory’s share worth is considerably above the GF Worth Line, the inventory could also be overvalued and have poor future returns. Conversely, if the inventory’s share worth is considerably beneath the GF Worth Line, the inventory could also be undervalued and have excessive future returns. On condition that Martin Marietta Supplies is pretty valued, the long-term return of its inventory is more likely to be near the speed of its enterprise progress.

Monetary Energy

Corporations with poor monetary energy pose a excessive threat of everlasting capital loss to buyers. To keep away from this, buyers should analysis and evaluation an organization’s monetary energy earlier than deciding to buy shares. Martin Marietta Supplies has a cash-to-debt ratio of 0.08, rating worse than 85.07% of 355 firms within the Constructing Supplies trade. The general monetary energy of Martin Marietta Supplies is 5 out of 10, indicating honest monetary energy.

Profitability and Development

Investing in worthwhile firms, particularly these with constant profitability over the long run, is much less dangerous. Martin Marietta Supplies has been worthwhile 10 over the previous 10 years. Over the previous twelve months, the corporate had a income of $6.50 billion and Earnings Per Share (EPS) of $15.24. Its working margin is 20.63%, which ranks higher than 87.29% of 362 firms within the Constructing Supplies trade. General, the profitability of Martin Marietta Supplies is ranked 9 out of 10, indicating robust profitability.

Development is a necessary issue within the valuation of an organization. Martin Marietta Supplies’s 3-year common income progress price is best than 64.59% of 353 firms within the Constructing Supplies trade. Its 3-year common EBITDA progress price is 12.4%, rating higher than 70.35% of 317 firms within the trade.

ROIC vs WACC

Evaluating an organization’s return on invested capital and the weighted price of capital is one other method to have a look at its profitability. Return on invested capital (ROIC) measures how nicely an organization generates money circulation relative to the capital it has invested in its enterprise. Then again, the weighted common price of capital (WACC) is the speed that an organization is anticipated to pay on common to all its safety holders to finance its property. For the previous 12 months, Martin Marietta Supplies’s return on invested capital is 7.56, and its price of capital is 8.9.

Conclusion

In brief, the inventory of Martin Marietta Supplies (NYSE:MLM) is estimated to be pretty valued. The corporate’s monetary situation is honest, and its profitability is powerful. Its progress ranks higher than 70.35% of 317 firms within the Constructing Supplies trade. To study extra about Martin Marietta Supplies inventory, you’ll be able to take a look at its 30-Yr Financials right here.

To search out out the high-quality firms which will ship above-average returns, please take a look at GuruFocus Excessive High quality Low Capex Screener.

This text first appeared on GuruFocus.