Ivan Bajic

Introduction

Nu Pores and skin (NYSE:NUS), a magnificence multilevel advertising firm, faces falling gross sales and margins. Their merchandise are costly, and the multilevel advertising mannequin is dangerous. Like Avon, Nu Pores and skin may battle. Their deal with increasing the multilevel advertising mannequin ignores the decline of this enterprise mannequin. Regardless of a possible vivid spot in manufacturing (Rhyz), the core enterprise is predicted to shrink in 2024. Total, I like to recommend promoting Nu Pores and skin inventory resulting from a bleak outlook and a much less promising future in multilevel advertising.

Present State of affairs

Nu Pores and skin is an organization that develops and sells magnificence and wellness merchandise by way of direct promoting, primarily person-to-person (multilevel advertising), and utilizing social media within the magnificence retailing and manufacturing industries. They function globally, with the US representing about 26% of their income. Along with their core enterprise, they put money into associated areas by way of Rhyz Inc. (primarily manufacturing capacities), contributing 11% of their income in 2023 and 13% in 4Q23.

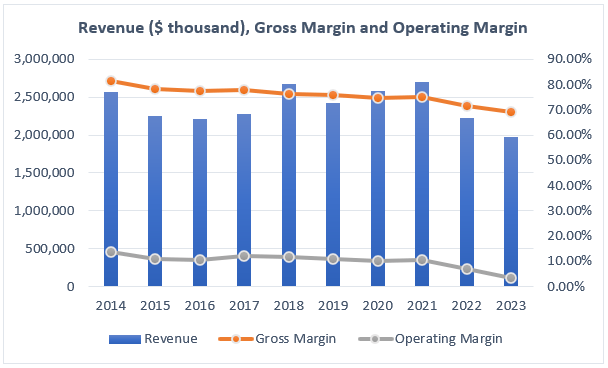

The corporate skilled flat gross sales between 2014 and 2021, however in 2022 and 2023, its income fell by -17.4% and -11.5%, respectively. Furthermore, even when income remained flat more often than not, its margin didn’t. The gross margin fell from 81.4% in 2014 to 68.9% in 2023; the working margin fell from 13.7% in 2014 to three.5% in 2023, shedding 1000 bps in lower than ten years.

Creator’s Elaboration with information from QuickFS

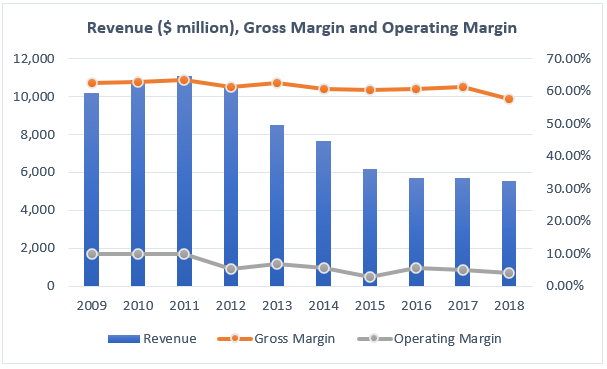

Nu Pores and skin’s scenario resembles the scenario of many different multilevel advertising firms, akin to Herbalife (HLF), Avon, Tupperware (TUP), and Medifast (MED). Essentially the most related firm was Avon, which was compelled to promote its US enterprise for $170 to Cerberus in 2015, and subsequently, the entire firm was acquired by Natura Co. in 2020. Analyzing the final years of Avon as a public firm, we discover a related sample in its income and margins.

Creator’s Elaboration with information from QuickFS

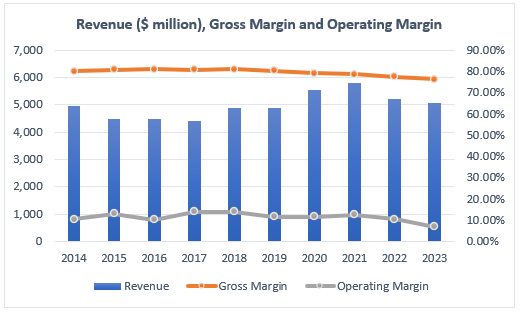

Moreover, Herbalife has additionally been struggling to make its income develop continuously, whereas its margins have been contracting within the earlier 4 years.

Creator’s Elaboration with information from QuickFS

The explanations behind the failure of most multilevel advertising firms are uncompetitive value construction in comparison with giant retailers, increased authorized danger, and low-quality merchandise in comparison with their costs.

First, Avon failed within the US due to the speedy progress of magnificence retailers with reasonably priced luxurious manufacturers, akin to Ulta Magnificence (ULTA) and Sephora, alongside non-specialty retailers incorporating magnificence merchandise to their cabinets, in keeping with Fortune. Moreover, analyzing a comparability between Nu Pores and skin’s value construction and Ulta Magnificence’s value construction, made by Fernando Batista on In search of Alpha, offers us a transparent image of how Ulta Magnificence can generate, on common, extra working earnings per income than Nu Pores and skin. Consequently, I feel the drawback in the fee construction may clarify why the margins began falling sharply within the earlier three years, as shoppers’ wallets had been squeezed by the excessive inflation, producing a extra acutely aware shopper; thus, from my standpoint, Nu Pores and skin is very weak to enterprise cycles.

Second, multilevel advertising has been and possibly will proceed to be uncovered to lawsuits, fines, and prohibitions in a number of world areas. As an example, resulting from restrictions, Nu Pores and skin modified its enterprise mannequin from multilevel advertising to retail promoting in China, after it paid $47 million. Moreover, within the US, we discover a number of lawsuits towards multilevel firms; for instance, in 2019, many firms with the identical enterprise mannequin had been concerned in authorized issues; a kind of firms was AdvoCare, which was banned from multilevel advertising and fined $150 million by the Federal Commerce Fee. Moreover, the FTC’s deal with policing inappropriate earnings claims and problematic compensation buildings and guaranteeing shopper safety may simply translate into authorized motion towards Nu Pores and skin if its practices are deemed to violate evolving interpretations of direct promoting and anti-pyramid legal guidelines. Examples abound: the FTC’s aggressive 2015 motion towards a multilevel advertising firm and the 2019 case the place an organization was barred from utilizing multilevel advertising mannequin altogether spotlight the potential penalties. Even seemingly minor infractions, just like the FTC’s 2020-2022 warnings towards COVID-19 product claims or deceptive earnings alternatives, show the company’s vigilance. The 2021 discover to Nu Pores and skin and over 1,100 different firms, outlining particular practices deemed misleading, additional underscores the potential for important civil penalties if FTC requirements aren’t met. The 2022 ANPR indicating a possible rule on earnings claims and the 2023 profitable lawsuit towards unlawful multi-level advertising applications solidify the FTC’s proactive stance.

Third, analyzing critiques from clients and dermatologists, Nu pores and skin merchandise don’t rank properly in comparison with different rivals. Within the case of dermatologists, the critiques on The Derm Assessment had been detrimental, acquiring 3.3 out of 5 stars as Nu Pores and skin merchandise had been considerably overpriced in comparison with rivals’ merchandise with related elements. Within the case of shoppers, I discovered combined critiques, on Amazon, many of the merchandise have greater than 4 out of 5 stars, however on Shopper Affairs, the merchandise solely get 3.4 out of 5 stars, with a mode of two stars. Moreover, on Trustpilot, they solely get 3.1 out of 5 stars. I discovered on Shopper Affairs, Trustpilot, and Quora allegations about overview manipulation by the corporate and people who promote the merchandise; even when this data can’t be confirmed, the incentives are there; if a vendor is dependent upon promoting Nu Pores and skin merchandise, she in all probability received’t give a nasty overview. Lastly, many critiques I learn complained about Nu Pores and skin merchandise being overpriced and low–high quality.

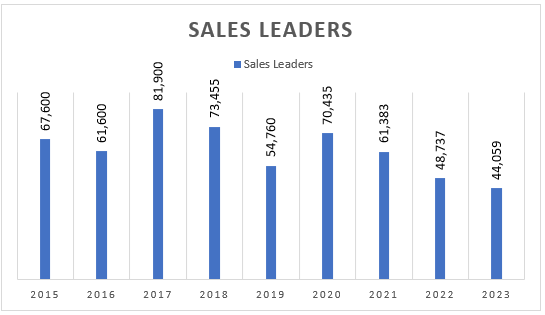

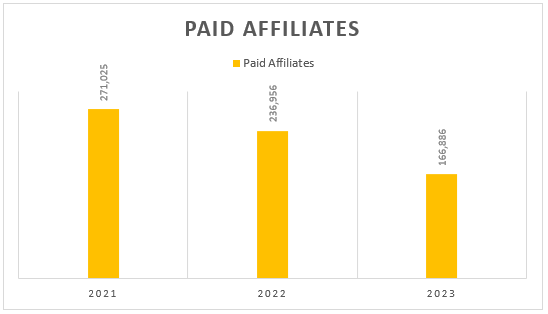

Following the disadvantages of multilevel advertising companies, anticipating a fall on this enterprise mannequin is believable. Nu Pores and skin has skilled fewer Gross sales Leaders and Paid Associates in earlier years. Having fewer distributors can have a detrimental impact within the coming years.

Creator’s Elaboration with information from Nu Pores and skin’s 10K Experiences Creator’s Elaboration with information from Nu Pores and skin’s 2023 10K Report

What to anticipate

Nu Pores and skin has lower its dividend to $0.06 quarterly just lately, and in the meanwhile of writing this text, it has a ahead dividend yield of 1.92% and a dividend payout ratio (primarily based on 2023 free money circulation) of 19.72%. The explanations behind the lower are the administration plan to achieve the Nu Imaginative and prescient 2025 targets, increase Rhyz enterprise, and increase to India and the mind well being market (in keeping with its final earnings name). Nonetheless, apart from Rhyz’s manufacturing capacities (which can produce different manufacturers), all the opposite initiatives are associated to the multilevel advertising technique that’s at the moment failing. From my perspective, the longer term doesn’t appear promising because the strategic plan doesn’t deal with the disadvantages of multilevel advertising and the worth points associated to its merchandise.

This capital allocation differs from different multilevel advertising firms, akin to Herbalife and Tupperware. Herbalife has centered on being a cannibal within the final ten years, decreasing its excellent shares from 181.6 million shares to 100 million shares. Tupperware paid dividends and made inventory repurchases earlier than experiencing difficulties in 2019 and so forth. Therefore, it looks as if Nu Pores and skin is searching for alternatives that won’t exist for multilevel advertising firms anymore as an alternative of specializing in returning capital to its shareholders by way of share buybacks and dividends. Nevertheless, increasing to a big market like India may hold the income from falling, as India’s progress offset the dangerous results of different markets. Moreover, even when increasing to the mind well being market may carry increased income, I doubt the success of those new merchandise primarily based on the dangerous critiques of the present merchandise; due to this fact, I feel they are going to have a low likelihood of success.

Nonetheless, I feel the Rhyz wager within the manufacturing trade may save the corporate from a declining enterprise mannequin; nevertheless, it doesn’t imply that the corporate will start to earn excessive returns if it shifts to a pure manufacturing participant as a result of it retains being a extremely aggressive trade with low pricing energy and important capital funding. Nonetheless, the administration expects Rhyz to be round 20-25% of gross sales by 2025. Subsequently, Nu Pores and skin will hold counting on a multilevel advertising technique.

On this sense, the administration expects a lower in gross sales in 2024 of roughly 8.59% if we take the center level of the steerage ($ 1.8 billion), which can be the analysts’ estimate. The lower in income is predicted even when the Rhyz enterprise continues to indicate robust progress, with 41% progress in the entire yr and 100% in 4Q23. Moreover, the administration expects Rhyz to develop at a double-digit fee within the following years. Consequently, the administration is predicted a decline within the income of its core enterprise even when macroeconomic circumstances are already enhancing.

However, the EPS in 2024 will probably be round $0.75 and $1.15, in keeping with the steerage, whereas analysts anticipate it to be round $1; due to this fact, Nu Pores and skin is buying and selling at a FWD P/E of roughly 12.64, which I consider is somewhat demanding given the dire outlook the corporate is dealing with and the numerous aggressive disadvantages it has. Nonetheless, evaluating it to its historic valuations, the corporate provides a reduction, because the final 5 years’ median P/E has been 17.63; nevertheless, the monetary efficiency of the corporate has deteriorated within the earlier yr, and it would not appear to enhance quickly, so it might be too optimistic to assume that the corporate will commerce once more at these multiples. Furthermore, evaluating Nu Pores and skin with some rivals within the trade and a few firms with the identical enterprise mannequin, we discover that firms like Ulta Magnificence, L’Oreal (OTCPK:LRLCF), and Estee Lauder (EL) commerce at excessive FWD P/E multiples of 20.58, 34.13, and 35.34, respectively. Nevertheless, I do not assume which means Nu Pores and skin has a substantial low cost, as the corporate additionally has important aggressive disadvantages that can impair its progress alternatives. Furthermore, Nu Pores and skin is buying and selling at a premium in comparison with different multilevel advertising firms, because the FWD P/E of Herbalife and Tupperware are 3.8 and 6.56, respectively, and the P/E of Medifast is 4.44.

Lastly, I feel the Rhyz enterprise may save the corporate from the sluggish dying of the multilevel advertising enterprise, however the transition will probably be sluggish, in keeping with administration estimates.

Conclusion

From my perspective, Nu Pores and skin is a ‘Promote.’ The corporate has extreme aggressive disadvantages that can in all probability impair its progress alternatives. The shortage of aggressive merchandise, the non-competitive value construction, and the excessive likelihood of lawsuits make Nu Pores and skin keep behind the competitors. Furthermore, multilevel advertising appears to be declining, as firms like Herbalife, Medifast, Tupperware, and Nu Pores and skin battle to stay aggressive out there, whereas Avon already failed. Nonetheless, I feel the Rhyz wager may transfer the corporate to a different enterprise mannequin the place it may earn higher returns and continue to grow. Nevertheless, the transition will probably be sluggish to an already aggressive market will probably be sluggish, so the returns will not be excessive and can take an excessive amount of time to be important. Lastly, increasing to India and the mind well being market may carry again income progress and enhance the outlook when carried out.

Editor’s Notice: This text covers a number of microcap shares. Please concentrate on the dangers related to these shares.